|

시장보고서

상품코드

1683871

유럽의 LFP 배터리 팩 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2029년)Europe LFP Battery Pack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2029) |

||||||

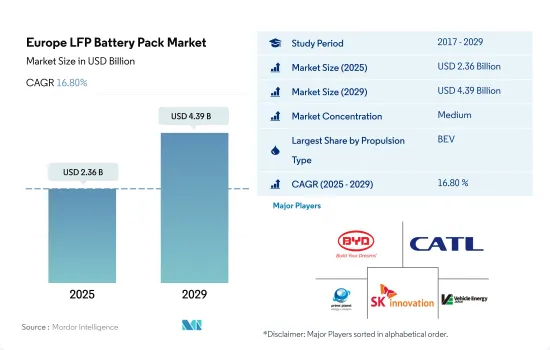

유럽의 LFP 배터리 팩 시장 규모는 2025년 23억 6,000만 달러, 2029년에는 43억 9,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2029년) CAGR은 16.80%로 성장할 것으로 예측됩니다.

유럽의 LFP 배터리 팩 시장은 BEV의 보급을 배경으로 강력한 성장이 전망

- 유럽에서 LFP 배터리 팩을 채택하고 판매하는 것은 현저한 성장 궤도를 따릅니다. ResearchAndMarkets의 보고서에 따르면 유럽의 LFP 배터리 팩 시장은 2021년부터 2026년까지 CAGR 14.1%로, 2026년에는 135억 달러에 달할 것으로 예상되고 있습니다. 이러한 성장의 배경에는 전기자동차에 대한 수요가 증가하고 신뢰성이 높고 고성능이며 저렴한 배터리 솔루션에 대한 요구가 있습니다.

- 유럽에서 LFP 배터리 팩에 대한 수요가 증가하고 있는 이유는 다른 유형의 배터리 팩에 비해 안전 수준이 높고, 수명 주기가 길고, 비용이 낮아지는 등 몇 가지 장점이 있기 때문입니다. 배터리 기술의 진보에 따라 LFP 배터리 팩의 밀도와 항속 거리가 향상되어 항속 거리의 연장과 전기자동차 전체의 성능 향상을 실현하고 있습니다. LFP 배터리 팩의 비용도 낮아져 소비자에게 보다 친숙한 존재가 되어 시장에서의 보급을 뒷받침하고 있습니다.

- 배터리기술의 연구개발에 엄청난 자금이 투입되고 있기 때문에 유럽의 LFP 배터리팩 산업에는 밝은 미래가 있습니다. 주요 목표는 LFP 배터리 팩의 성능을 더욱 향상시키고, 경량화하고, 에너지 밀도를 높이는 것입니다. LFP 배터리 팩은 시장에서의 경쟁력을 더욱 향상시켜 가격 인하에 기여할 것으로 보입니다. 2023-2029년 예상 기간 동안 전기자동차의 보급이 진행되고 지속 가능한 에너지 솔루션이 요구됨에 따라 LFP 배터리 팩 수요는 유럽에서 증가할 것으로 예상됩니다.

독일이 유럽의 LFP 배터리 팩 시장의 주요 기업으로서 현저한 성장을 이룩

- 유럽 전기자동차용 LFP 배터리 팩 시장은 역동적인 성장 시장입니다. EV의 보급이 진행되고 배터리 팩의 비용이 저하되고 있는 것을 배경으로, 시장은 앞으로도 계속 성장할 것으로 예상됩니다. 위의 요인 외에도 몇 가지 요인이 향후 몇 년동안 유럽 전기자동차 배터리 팩 시장의 성장을 가속할 것으로 예상됩니다.

- 독일은 이 시장의 주요 기업으로서 두드러지며 지난 몇 년간 현저한 가격 상승을 보이고 있습니다. 이러한 성장은 전기자동차에 대한 정부의 지원, EV에 대한 소비자 수요 증가, 배터리 기술의 발전 등 다양한 요인에 기인합니다. 독일의 견조한 자동차 산업은 선도적인 자동차 제조 업체의 전기자동차 생산에 대한 많은 투자와 함께 배터리 팩 수요 급증에 크게 기여하고 있습니다.

- 유럽의 또 다른 주요 국가인 프랑스는 배터리 팩 시장의 현저한 성장을 목격했습니다. 호의적인 정책과 인센티브를 통한 전기차 도입을 촉진하는 프랑스의 헌신은 배터리 팩 시장의 성장을 가속하는데 중요한 역할을 합니다. 이탈리아는 독일과 프랑스에 비해 성장이 둔화되고 있는 것, 배터리 팩 시장은 여전히 상승세입니다. 전기자동차에 대한 소비자의 의식 증가, 정부의 장려책, 기술의 진보 등의 요인이 이탈리아에서 시장 성장에 기여하고 있습니다. 전기자동차 수요가 계속 증가함에 따라 배터리 팩은 이탈리아에서 지속 가능한 이동성으로의 전환을 지원하는 중요한 역할을 수행할 것으로 기대됩니다.

유럽의 LFP 배터리 팩 시장 동향

Toyota Group이 유럽 전기자동차 시장을 선도하고 Renault, Tesla, Kia, BMW가 이에 이어

- 유럽 각국의 전기자동차 시장은 크게 성장하고 있어 다수의 기업이 사업을 전개하고 있지만, 2022년에는 시장의 50% 이상을 차지하는 대기업 5사에 의해 크게 견인되고 있습니다. 이러한 기업에는 Toyota Group, Kia, Renault, Tesla, Kia, Volkswagen이 포함됩니다. Toyota Group은 유럽에서 가장 큰 전기자동차 판매 회사이며 전기자동차 시장에서 약 14.84%의 점유율을 차지하고 있습니다. 이 회사는 유럽 각국의 고객 수요 및 공급에 대응하는 강력한 공급 및 유통 네트워크를 가지고 있습니다. Renault는 전기자동차 시장에서 광범위한 제품 포트폴리오를 제공합니다.

- Renault 시장 점유율은 약 7.47%로 유럽 전체에서 전기차 판매 2위를 차지하고 있습니다. Renault의 브랜드 이미지는 높고, 재무 상황도 양호합니다. Nissan 등 우량 브랜드와의 제휴와 전략적 파트너십을 맺고 있습니다. 전기차 판매 점유율 3위의 6.71%를 기록한 것은 Tesla입니다. Tesla는 첨단 기술 혁신에 주력하고 있으며 배터리를 포함한 전기자동차 부품 제조업체와 강력한 전략적 제휴 관계를 맺고 있습니다.

- 유럽 EV 판매 대수 4위는 Kia로 시장 점유율의 약 6.26%를 차지하고 있습니다. 이 회사는 다양한 유형의 고객을 위한 다양한 제품 유형을 제공하며 다른 브랜드와 비교하여 예산에 따라 다양한 옵션을 제공합니다. 유럽 EV 시장의 5위는 BMW로 약 6.14% 시장 점유율을 유지하고 있습니다. 유럽 국가에서 EV를 판매하는 다른 기업은 Hyundai, Mercedes-Benz, BMW, Audi, Ford 등이 있습니다.

Tesla와 Renault는 2022년 유럽에서 EV가 널리 판매된 결과 배터리 팩 수요에 가장 기여하고 있습니다.

- 전기자동차 수요는 지난 몇 년동안 유럽의 모든 지역에서 극적으로 증가했습니다. 전기자동차는 현재 유럽 도로에 더 많이 보급되고 있습니다. 전기자동차 구매에 대한 소비자의 관심은 지역과 국가에 따라 다르지만, 이 지역의 전기자동차 2대 시장인 독일과 영국에서는 SUV가 가장 인기 있는 유형의 전기자동차입니다. 쾌적한 이동수단에 대한 관심 증가와 SUV는 세단보다 실내가 넓기 때문에 유럽 각국에서는 전동 SUV 수요가 세단을 웃돌고 있습니다.

- 소비자에 의한 소형 SUV 구매 대수는 유럽 전역에서 극적으로 증가하고 있습니다. Tesla 모델 Y는 완전한 전기 모터, 5성급 NCAP 안전 인증, 최대 7인승의 넓은 좌석, 장거리 주행 등의 특징을 갖추고 있습니다. 2022년에는 영국과 독일 등 여러 주요 유럽 시장에서 가장 인기 있는 모델 중 하나가 되었습니다. Renault Arkana는 풀 하이브리드 엔진을 탑재하고 있으며, 그 연비의 장점과 경쟁력있는 가격 설정에 의해 프랑스 등 유럽 여러 국가의 고객으로부터 강한 판매 반응을 얻고 있습니다.

- Captur은 하이브리드와 플러그인 하이브리드의 파워트레인을 제공하고 구매자를 끌어들이는 많은 기능을 가득 채우기 때문에 2022년 유럽 국가에서 가장 팔린 Renault 중 하나가 되었습니다. 유럽 EV 시장에는 다양한 국제 브랜드의 전기 SUV와 세단도 있습니다. 일반적인 자동차 중 하나는 Toyota Yaris 와 Ford Kuga로, 2022년에는 호조로 팔렸습니다. 유럽 EV 시장에서 경쟁 관계에 있는 다른 자동차로는 Fiat 500, Toyota Yaris Cross 등이 있습니다.

유럽의 LFP 배터리 팩 산업 개요

유럽의 LFP 배터리 팩 시장은 상위 5곳에서 56.41%를 차지하며 완만하게 통합되어 있습니다. 이 시장 주요 기업은 다음과 같습니다. BYD Company Ltd., Contemporary Amperex Technology(CATL), Prime Planet Energy & Solutions Inc., SK Innovation and Vehicle Energy Japan Inc.(알파벳순).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 전기자동차 판매 대수

- OEM별 전기자동차 판매 대수

- 판매 LINE EV 모델

- 선호되는 배터리 화학을 가진 OEM

- 배터리 팩 가격

- 배터리 재료 비용

- 각 배터리 화학의 가격표

- 누가 누구에게 공급하는지

- EV 배터리의 용량과 효율

- EV의 발매 모델수

- 규제 프레임워크

- 벨기에

- 프랑스

- 독일

- 헝가리

- 폴란드

- 영국

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 차체 유형

- 버스

- LCV

- M&HDT

- 승용차

- 추진 유형

- BEV

- PHEV

- 용량

- 15-40 kWh

- 40-80 kWh

- 80kWh 이상

- 15kWh 미만

- 배터리 형상

- 원통형

- 가방

- 각형

- 방식

- 레이저

- 와이어

- 컴포넌트

- 애노드

- 캐소드

- 전해액

- 세퍼레이터

- 재료 유형

- 코발트

- 리튬

- 망간

- 천연 흑연

- 니켈

- 기타 재료

- 국가

- 프랑스

- 독일

- 헝가리

- 이탈리아

- 폴란드

- 스웨덴

- 영국

- 기타 유럽

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- BMZ Batterien-Montage-Zentrum GmbH

- BYD Company Ltd.

- Contemporary Amperex Technology Co. Ltd.(CATL)

- LG Energy Solution Ltd.

- NorthVolt AB

- Panasonic Holdings Corporation

- Prime Planet Energy & Solutions Inc.

- SAIC Volkswagen Power Battery Co. Ltd.

- Samsung SDI Co. Ltd.

- SK Innovation Co. Ltd.

- SVOLT Energy Technology Co. Ltd.(SVOLT)

- TOSHIBA Corp.

- Vehicle Energy Japan Inc.

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Europe LFP Battery Pack Market size is estimated at 2.36 billion USD in 2025, and is expected to reach 4.39 billion USD by 2029, growing at a CAGR of 16.80% during the forecast period (2025-2029).

The European LFP battery pack market is expected to witness strong growth on the back of BEV adoption

- The adoption and sales of LFP battery packs in Europe have seen a significant growth trajectory. According to a report by ResearchAndMarkets, the market for LFP battery packs in Europe is expected to reach USD 13.5 billion by 2026, with a CAGR of 14.1% from 2021 to 2026. The growth can be attributed to the increasing demand for electric vehicles and the need for reliable, high-performance, and affordable battery solutions.

- The increasing demand for LFP battery packs in Europe is due to their several benefits, including higher safety levels, longer life cycles, and lower cost compared to other types of battery packs. With advancements in battery technology, the density and range of LFP battery packs have been increasing, providing longer ranges and improving the overall performance of electric vehicles. The cost of LFP battery packs has also been decreasing, making them more accessible to consumers and boosting their adoption in the market.

- Due to substantial expenditures being made in the study and development of battery technologies, the LFP battery pack industry in Europe has a bright future. The main goals are to further enhance the performance, decrease the weight, and boost the energy density of LFP battery packs. LFP battery packs will become even more competitive on the market and, as a result of this, help to lower their price. During the anticipated period of 2023-2029, demand for LFP battery packs is anticipated to increase in Europe as a result of the growing adoption of electric cars and the desire for sustainable energy solutions.

Germany emerges as a key player in the European LFP battery pack market with remarkable growth

- The European electric vehicle LFP battery pack market is a dynamic and growing market. The market is expected to continue to grow in the coming years, driven by the increasing adoption of EVs and the declining cost of battery packs. In addition to the factors mentioned above, several other factors are expected to drive the growth of the European electric vehicle battery pack market in the coming years.

- Germany stands out as a leading player in the market, with a remarkable increase in value over the years. This growth can be attributed to various factors, such as government support for electric vehicles, rising consumer demand for EVs, and advancements in battery technology. Germany's robust automotive industry, combined with substantial investments by major automakers in electric vehicle production, has significantly contributed to the surge in demand for battery packs.

- France, another prominent European country, has witnessed notable growth in the battery pack market. France's commitment to promoting the adoption of electric vehicles through favorable policies and incentives has played a significant role in driving the growth of the battery pack market. Italy, while exhibiting slower growth compared to Germany and France, has still experienced an upward trend in the battery pack market. Factors such as increasing consumer awareness of electric vehicles, government incentives, and technological advancements have contributed to the market's growth in Italy. As the demand for electric vehicles continues to rise, battery packs are expected to play a crucial role in supporting the transition toward sustainable mobility in Italy.

Europe LFP Battery Pack Market Trends

TOYOTA GROUP LEADS THE EUROPEAN EV MARKET, FOLLOWED BY RENAULT, TESLA, KIA, AND BMW

- The market for electric vehicles in various European countries is growing significantly, with numerous players operating, but it is largely driven by five major companies, which held more than 50% of the market in 2022. These companies include Toyota Group, Kia, Renault, Tesla, Kia, and Volkswagen. Toyota Group is the largest seller of electric vehicles in Europe, accounting for around 14.84% share of the electric car market. The company has a strong supply and distribution network catering to the demand and supply of customers in various European countries. The company has a wide product portfolio offering in the EV market.

- Renault holds a market share of around 7.47%, making it the second-largest seller of electric vehicles across Europe. The company has a good brand image and a strong financial position. The company has alliances and strategic partnerships with good brands such as Nissan. The 3rd highest market share, 6.71%, for electric vehicle sales was recorded by Tesla. The business focuses on cutting-edge innovations and has solid strategic alliances with producers of several EV parts, including batteries.

- The 4th largest place in European EV sales is Kia, accounting for around 6.26% of the market share. The company has wide product offerings for various types of customers with various budget-friendly options compared to other brands. The 5th largest player operating in the European EV market is BMW, maintaining its market share at around 6.14%. Some of the other players selling EVs in various European countries include Hyundai, Mercedes-Benz, BMW, Audi, and Ford.

Tesla and Renault are the largest contributors to the demand for battery packs, as a result of the widespread sale of EVs in Europe in 2022

- The demand for electric vehicles has dramatically increased during the past several years in every part of Europe. Electric vehicles are now more prevalent on European roadways. Although consumer interest in buying electric vehicles varies by area and by country, SUVs are the most popular type of electric vehicle in Germany and the United Kingdom, the region's two biggest markets for electric vehicles. The demand for electric SUVs is outpacing that for sedans in various European countries due to the increased interest in comfortable transportation and the fact that SUVs are roomier than sedans.

- The number of compact SUVs purchased by consumers has increased dramatically across Europe. The Tesla Model Y offers a fully electric motor, a 5-star NCAP safety certification, spacious seating for up to 7 passengers, a long-range, and other features. It became one of the most popular models in several major European markets, including the United Kingdom and Germany, in 2022. The Renault Arkana provides a full hybrid engine, which has received a strong sales reaction from customers in several European nations like France due to its fuel efficiency and competitive pricing.

- Captur was one of the best sellers from Renault in the European countries in 2022, owing to its offering of a hybrid and a plug-in hybrid powertrain, and is packed with lots of features attracting buyers. The European EV market also features a variety of electric SUVs and sedans from various international brands. One of the common cars is the Toyota Yaris and Ford Kuga, which recorded good sales in 2022. Other cars in the European EV market that are in the competition include the Fiat 500 and Toyota Yaris Cross.

Europe LFP Battery Pack Industry Overview

The Europe LFP Battery Pack Market is moderately consolidated, with the top five companies occupying 56.41%. The major players in this market are BYD Company Ltd., Contemporary Amperex Technology Co. Ltd. (CATL), Prime Planet Energy & Solutions Inc., SK Innovation Co. Ltd. and Vehicle Energy Japan Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Electric Vehicle Sales

- 4.2 Electric Vehicle Sales By OEMs

- 4.3 Best-selling EV Models

- 4.4 OEMs With Preferable Battery Chemistry

- 4.5 Battery Pack Price

- 4.6 Battery Material Cost

- 4.7 Price Chart Of Different Battery Chemistry

- 4.8 Who Supply Whom

- 4.9 EV Battery Capacity And Efficiency

- 4.10 Number Of EV Models Launched

- 4.11 Regulatory Framework

- 4.11.1 Belgium

- 4.11.2 France

- 4.11.3 Germany

- 4.11.4 Hungary

- 4.11.5 Poland

- 4.11.6 UK

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Body Type

- 5.1.1 Bus

- 5.1.2 LCV

- 5.1.3 M&HDT

- 5.1.4 Passenger Car

- 5.2 Propulsion Type

- 5.2.1 BEV

- 5.2.2 PHEV

- 5.3 Capacity

- 5.3.1 15 kWh to 40 kWh

- 5.3.2 40 kWh to 80 kWh

- 5.3.3 Above 80 kWh

- 5.3.4 Less than 15 kWh

- 5.4 Battery Form

- 5.4.1 Cylindrical

- 5.4.2 Pouch

- 5.4.3 Prismatic

- 5.5 Method

- 5.5.1 Laser

- 5.5.2 Wire

- 5.6 Component

- 5.6.1 Anode

- 5.6.2 Cathode

- 5.6.3 Electrolyte

- 5.6.4 Separator

- 5.7 Material Type

- 5.7.1 Cobalt

- 5.7.2 Lithium

- 5.7.3 Manganese

- 5.7.4 Natural Graphite

- 5.7.5 Nickel

- 5.7.6 Other Materials

- 5.8 Country

- 5.8.1 France

- 5.8.2 Germany

- 5.8.3 Hungary

- 5.8.4 Italy

- 5.8.5 Poland

- 5.8.6 Sweden

- 5.8.7 UK

- 5.8.8 Rest-of-Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 BMZ Batterien-Montage-Zentrum GmbH

- 6.4.2 BYD Company Ltd.

- 6.4.3 Contemporary Amperex Technology Co. Ltd. (CATL)

- 6.4.4 LG Energy Solution Ltd.

- 6.4.5 NorthVolt AB

- 6.4.6 Panasonic Holdings Corporation

- 6.4.7 Prime Planet Energy & Solutions Inc.

- 6.4.8 SAIC Volkswagen Power Battery Co. Ltd.

- 6.4.9 Samsung SDI Co. Ltd.

- 6.4.10 SK Innovation Co. Ltd.

- 6.4.11 SVOLT Energy Technology Co. Ltd. (SVOLT)

- 6.4.12 TOSHIBA Corp.

- 6.4.13 Vehicle Energy Japan Inc.

7 KEY STRATEGIC QUESTIONS FOR EV BATTERY PACK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms