|

시장보고서

상품코드

1750328

블로우 스트레치 포장 필름 시장 : 시장 기회, 성장 촉진요인, 업계 동향 분석, 예측(2025-2034년)Blown Stretch Packaging Films Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

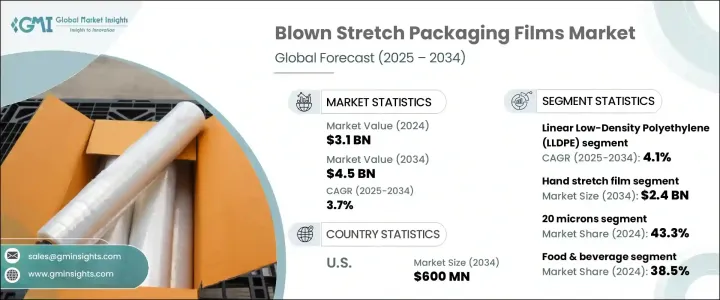

세계의 블로우 스트레치 포장 필름 시장은 2024년에는 31억 달러로 평가되었고, CAGR 3.7%로 성장할 전망이며, 2034년에는 45억 달러에 이를 것으로 추정되고 있습니다.

이 성장은 주로 식음료 분야를 필두로 하는 다양한 포장 용도에서 수요 증가가 견인하고 있습니다. 내구성이 뛰어나고 유연하며 경량인 포장 재료에 대한 요구가 높아지는 가운데 블로우 스트레치 필름이 큰 지지를 얻고 있습니다. 이러한 필름은 우수한 하중 안정성, 제품 보호, 비용 대비 효과를 제공하기 때문에 포장의 완전성과 효율이 중요한 산업에서 필수적인 것이 되고 있습니다. 오랜 세월에 걸쳐, 경제적 및 정치적 요인도 시장 정세의 형성에 한 몫 해 왔습니다. 무역 제한 및 관세의 변경은 특히 투입 비용의 상승에 의해 공급망을 압박하고 있습니다. 이에 대응하기 위해 제조업체는 지정학적 리스크를 경감하고 사업의 계속성을 확보하기 위해 지역에 특화된 생산 전략을 채택하도록 되어 있습니다. 이 시프트는 기업이 시장 역학에 신속하게 적응할 수 있는 지역에 뿌리를 둔 생태계를 구축함으로써 조업 비용을 절감하고 공급망을 확보하며 이익률을 지키는 데 도움이 됩니다.

소재의 유형은 시장의 진화에 중요한 역할을 하고 있습니다. 직쇄상 저밀도 폴리에틸렌(LLDPE)은 높은 인장강도, 유연성, 내펑크성 등의 우수한 기계적 특성으로 인해 시장의 대부분을 차지하고 있습니다. 이러한 특성으로 인해 LLDPE는 스트레치 필름 제조, 특히 내구성을 해치지 않으면서 재료 사용량을 줄이기 위해 얇은 필름이 필요한 경우에 바람직한 선택지가 되고 있습니다. LLDPE 분야는 2034년까지 CAGR 4.1%로 성장할 것으로 예측되고 있는데, 이는 물류나 소비재 등의 분야에서 고성능의 비용 효율이 높은 포장 솔루션에 대한 기호가 높아지고 있음을 반영하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 31억 달러 |

| 예측 금액 | 45억 달러 |

| CAGR | 3.7% |

제품 유형별로는 핸드 스트레치 필름, 머신 스트레치 필름, 스페셜티 유형이 있습니다. 이 중, 핸드 스트레치 필름은, 그 비용 대비 효과와 높은 범용성으로부터 지지를 모으고 있습니다. 핸드 스트레치 필름 분야는, 수작업에 의한 포장에 의지하고 있는 중소기업이나 창고 업무에서의 이용이 증가하고 있는 것을 배경으로, 2034년까지 24억 달러에 달할 것으로 예측되고 있습니다. 이 필름들은 특히 자동화 인프라가 최소한인 시장에서 소량 포장 요구에 실용적인 솔루션을 제공합니다.

두께도 수요에 영향을 미치는 중요한 매개 변수입니다. 2024년 시장 점유율은 두께 20미크론까지의 필름이 43.3%를 차지했습니다. 이 부문은 더 가벼운 상품을 포장하기 위해 더 얇은 필름에 눈을 돌리는 산업이 늘어남에 따라 확대되고 있습니다. 보다 얇은 필름을 선호함으로써 포장 폐기물의 삭감, 운송 비용의 삭감, 지속 가능성에 대한 대처가 지원됩니다.

최종 이용 산업 세분화에서는 식음료 분야가 압도적인 존재감을 나타내고 있으며, 2024년 시장 점유율은 38.5%였습니다. 블로우 스트레치 필름은 습기나 물리적 손상으로부터 보호하고 제품의 유통 기한을 늘림으로써 이 업계에서 중요한 역할을 하고 있습니다. 보관 중이나 운송 중에 안전하고 위생적인 포장을 지원하는 그 능력은 신선품에 매우 적합합니다. 소비자들이 안전하고 편리한 포장을 요구하기 때문에 이 분야에서는 블로우 스트레치 필름의 채택이 계속 증가하고 있습니다.

유통 채널도 시장 역학을 형성하고 있으며, 직접 판매가 2024년의 총 점유율의 52%를 차지해 선도했습니다. 직판을 통해 제조사는 필름 두께, 인장 강도, 시각적 속성 등 특정 고객 요건에 맞는 맞춤형 패키징 솔루션을 제공할 수 있습니다. 이 접근 방식은 고객과의 관계를 강화하고 원활한 커뮤니케이션을 가능하게 하며 더 나은 서비스 및 제품 지원을 보장합니다.

지역별로는 미국이 강력한 성장을 이룰 것으로 예상되고 있으며, 2034년까지 시장은 6억 달러에 달할 것으로 예측되고 있습니다. 특히 전자상거래의 확대 및 안전하고 효율적인 제품 배송에 대한 소비자의 기대가 높아지면서 고성능 식품 포장 재료에 대한 수요가 높아지고 있습니다. 그 결과, 이 시장에서는, 제품의 완전성을 확보해, 증대하는 물류 요구를 서포트하기 위해서, 포장 솔루션의 기술 혁신이 진행되고 있습니다.

블로우 스트레치 패키징 필름 시장의 경쟁 환경은 여전히 치열하며, 대기업은 품질, 혁신 및 지속가능성으로 경쟁하고 있습니다. 기업은 환경 기준 및 소비자의 취향을 충족시키기 위해 생분해성 필름과 다층 필름 기술 개발에 많은 투자를 하고 있습니다. 또한 기업은 시장에서의 존재감을 강화하고 기술력을 향상시키기 위해 전략적 합병, 인수, 지역 확대에 주력하고 있습니다. 또한 공급망의 효율성을 높이고 안전성을 확보하기 위해 RFID 통합 및 온도 모니터링과 같은 스마트 포장 솔루션에 대한 관심도 높아지고 있습니다. 의약품, 물류 및 소비재와 같은 대상 산업에 대한 맞춤화는 이러한 진화 시장에서 차별화 요인으로 점점 더 중요해지고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 트럼프 정권의 관세 분석

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에 대한 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망 및 향후 검토 사항

- 무역에 미치는 영향

- 업계에 미치는 영향요인

- 성장 촉진요인

- 한랭 지역에서 항공 교통량 증가

- 엄격한 항공 안전 규제

- 제빙 기술의 진보

- 공항 인프라 확장

- 기후 변화 및 가혹한 겨울

- 업계의 잠재적 위험 및 과제

- 높은 운용 및 보수 비용

- 환경 및 규제에 대한 우려

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술의 상황

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 핸드 스트레치 필름

- 기계 스트레치 필름

- 특수 스트레치 필름

제6장 시장 추계 및 예측 : 재료별(2021-2034년)

- 주요 동향

- 선형 저밀도 폴리에틸렌(LLDPE)

- 저밀도 폴리에틸렌(LDPE)

- 고밀도 폴리에틸렌(HDPE)

- 폴리프로필렌(PP)

- 기타

제7장 시장 추계 및 예측 : 두께별(2021-2034년)

- 주요 동향

- 최대 20 미크론

- 21-40 미크론

- 40 미크론 이상

제8장 시장 추계 및 예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 식품 및 음료

- 공업용 포장

- 소비재

- 의약품

- 기타

제9장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접 판매

- 판매자 및 도매업체

- 온라인 채널

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Berry Global Inc.

- AEP Industries Inc.

- Amcor Plc

- Coveris Holdings SA

- DUO PLAST AG

- Eurofilms Extrusion Ltd

- FlexSol Packaging Corp.

- Integrated Packaging Group Pty Ltd

- Intertape Polymer Group Inc.

- Manuli Stretch SpA

- Megaplast India Pvt. Ltd.

- Mondi Group

- Paragon Films Inc.

- Polifilm GmbH

- RKW Group

- Sealed Air Corporation

- Sigma Plastics Group

- Trioplast Industrier AB

The Global Blown Stretch Packaging Films Market was valued at USD 3.1 billion in 2024 and is estimated to grow at a CAGR of 3.7% to reach USD 4.5 billion by 2034. This growth is primarily driven by increasing demand across various packaging applications, with the food and beverage sector at the forefront. As the need for durable, flexible, and lightweight packaging materials rises, blown stretch films have gained significant traction. These films offer superior load stability, product protection, and cost-effectiveness, making them essential in industries where packaging integrity and efficiency are vital. Over the years, economic and political factors have also played a role in shaping the market landscape. Trade restrictions and tariff changes have pressured the supply chain, particularly due to rising input costs. In response, manufacturers are adopting region-specific production strategies to reduce geopolitical risks and ensure business continuity. This shift helps companies lower operational costs, secure supply chains, and protect their profit margins by building localized ecosystems that can quickly adapt to market dynamics.

Material type plays a vital role in the market's evolution. Linear Low-Density Polyethylene (LLDPE) holds a significant portion of the market due to its outstanding mechanical properties, such as higher tensile strength, flexibility, and puncture resistance. These features make LLDPE a preferred choice for stretch film manufacturing, especially when thinner films are required to reduce material usage without compromising durability. The LLDPE segment is forecast to grow at a CAGR of 4.1% by 2034, reflecting the rising preference for high-performance and cost-efficient packaging solutions in sectors like logistics and consumer goods.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.1 Billion |

| Forecast Value | $4.5 Billion |

| CAGR | 3.7% |

In terms of product types, the market includes hand stretch films, machine stretch films, and specialty variants. Among these, hand stretch films are gaining traction due to their cost-effectiveness and versatility. The hand stretch film segment is projected to reach USD 2.4 billion by 2034, fueled by increasing usage among small to medium businesses and warehousing operations that rely on manual wrapping. These films provide a practical solution for low-volume packaging needs, especially in markets with minimal automation infrastructure.

Thickness is another key parameter influencing demand. Films with up to 20 microns in thickness accounted for a market share of 43.3% in 2024. This segment is expanding as more industries turn to thinner films to wrap lighter goods. The preference for lower thickness helps reduce packaging waste, cut transportation costs, and support sustainability efforts, which are increasingly important in modern supply chains.

The end-use industry segmentation shows a dominant presence in the food and beverage sector, which held a 38.5% market share in 2024. Blown stretch films serve a crucial role in this industry by offering protection against moisture and physical damage, extending product shelf life. Their ability to support secure and hygienic packaging during storage and transit makes them highly suitable for perishable goods. As consumers increasingly demand safe and convenient packaging, the adoption of blown stretch films continues to rise in this sector.

Distribution channels also shape the market dynamics, with direct sales leading the way by accounting for 52% of the total share in 2024. Direct sales allow manufacturers to provide customized packaging solutions tailored to specific customer requirements such as film thickness, tensile strength, or visual attributes. This approach strengthens client relationships and enables seamless communication, ensuring better service and product support.

In the regional landscape, the United States is expected to witness strong growth, with its market projected to hit USD 600 million by 2034. The demand for high-performance food packaging materials is rising, particularly due to expanding e-commerce and increased consumer expectations for safe and efficient product delivery. As a result, the market is seeing increased innovation in packaging solutions to ensure product integrity and support growing logistical needs.

The competitive environment in the blown stretch packaging films market remains intense, with leading players competing on quality, innovation, and sustainability. Companies are heavily investing in developing biodegradable and multi-layer film technologies to meet environmental standards and consumer preferences. In addition, firms are focusing on strategic mergers, acquisitions, and regional expansions to strengthen their market presence and improve technological capabilities. There is also growing interest in smart packaging solutions, including RFID integration and temperature monitoring, to enhance supply chain efficiency and ensure safety. Customization for targeted industries like pharmaceuticals, logistics, and consumer goods is becoming increasingly important as a differentiating factor in this evolving market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1.1 Supply chain reconfiguration

- 3.2.4.1.2 Pricing and product strategies

- 3.2.4.1.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth

- 3.3.1.1.1 Growing air traffic in cold regions

- 3.3.1.1.2 Stringent aviation safety regulations

- 3.3.1.1.3 Advancements in de-icing technologies

- 3.3.1.1.4 Expansion of airport infrastructure

- 3.3.1.1.5 Climate variability and severe winters

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High operational and maintenance costs

- 3.3.2.2 Environmental and regulatory concerns

- 3.3.1 Growth

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 (USD Billion & kilo tons)

- 5.1 Key trends

- 5.2 Hand stretch film

- 5.3 Machine stretch film

- 5.4 Specialty stretch film

Chapter 6 Market Estimates and Forecast, By Material Type, 2021 – 2034 (USD Billion & kilo tons)

- 6.1 Key trends

- 6.2 Linear low-density polyethylene (LLDPE)

- 6.3 Low-density polyethylene (LDPE)

- 6.4 High-density polyethylene (HDPE)

- 6.5 Polypropylene (PP)

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Thickness, 2021-2034 (USD Billion & kilo tons)

- 7.1 Key trends

- 7.2 Up to 20 microns

- 7.3 21–40 microns

- 7.4 Above 40 microns

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Billion & kilo tons)

- 8.1 Key trends

- 8.2 Food & beverage

- 8.3 Industrial packaging

- 8.4 Consumer goods

- 8.5 Pharmaceuticals

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 (USD Billion & kilo tons)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Distributors/wholesalers

- 9.4 Online channels

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion & kilo tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Berry Global Inc.

- 11.2 AEP Industries Inc.

- 11.3 Amcor Plc

- 11.4 Coveris Holdings S.A.

- 11.5 DUO PLAST AG

- 11.6 Eurofilms Extrusion Ltd

- 11.7 FlexSol Packaging Corp.

- 11.8 Integrated Packaging Group Pty Ltd

- 11.9 Intertape Polymer Group Inc.

- 11.10 Manuli Stretch S.p.A.

- 11.11 Megaplast India Pvt. Ltd.

- 11.12 Mondi Group

- 11.13 Paragon Films Inc.

- 11.14 Polifilm GmbH

- 11.15 RKW Group

- 11.16 Sealed Air Corporation

- 11.17 Sigma Plastics Group

- 11.18 Trioplast Industrier AB